How to Retire on $2 Million: Answers to the Questions People Actually Ask

Written By Michael Hart | June 11, 2026

If you have $2 million saved for retirement, you are probably asking a very specific question:

“Can I really afford to retire?”

The honest answer is: maybe — but the answer depends far more on your spending, taxes, healthcare costs, and expectations than the retirement industry often admits.

Many retirement articles oversimplify the conversation. They throw around blanket rules and generic projections without asking the questions that actually determine whether retirement works in real life.

A transparent, flat-fee, or advice-only financial advisor would usually approach the conversation differently. Instead of starting with investment products or portfolio performance, they typically start with your life, your cash flow, and your goals.

Below are the questions that matter most if you are trying to determine whether $2 million is enough to retire comfortably.

But first - a little background.

Hello, I’m Michael Hart, an advice-only financial planner serving Princeton, New Jersey and clients nationwide. My goal is to help individuals and families make informed financial decisions without product sales, commissions, or asset-based fees.

That means my recommendations are designed around your best interests—not around selling investments or insurance products.

And also…

Here are some blogs we’ve written on the subject of financial advice, which you may wish to read.

Buying a House Probably isn’t a Good Investment

Now let’s get on with it!

Is $2 Million Enough to Retire?

For many people, yes.

For others, not even close.

The most important variable is not the size of the portfolio itself. It is how much you spend relative to the portfolio.

A household spending $70,000 annually may have a very different retirement outcome than a household spending $220,000 annually, even if both have the exact same investment balance.

Here is a rough framework many planners would consider:

Spending $60,000–$80,000 per year → retirement may be very achievable

Spending $100,000–$140,000 per year → retirement may still work, but planning becomes more important

Spending $180,000+ annually → sustainability risks increase significantly unless additional income exists

This is why transparent advisors often begin retirement planning with spending analysis rather than investment returns.

How Much Income Can a $2 Million Portfolio Generate?

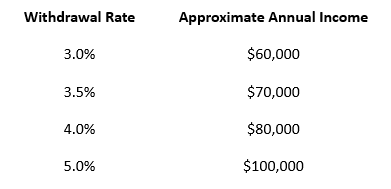

Many retirement discussions begin with withdrawal rates.

A commonly referenced guideline is the 4% rule.

That suggests a starting withdrawal of approximately $80,000 annually before taxes.

But this is where nuance matters.

The 4% guideline is not a guarantee. Some retirees may need a more conservative approach, while others may be able to spend more flexibly depending on market conditions and other income sources.

An advice-only planner may instead recommend:

3% withdrawal rate for highly conservative retirees

3.5%–4% for many households

Flexible adjustments during poor market periods

Here is what that may look like:

The key point is this:

$2 million does not automatically mean unlimited spending.

Does Social Security Make a Big Difference?

Yes — often a massive difference.

Many people underestimate how much guaranteed income changes retirement math.

For example, a married couple receiving combined Social Security benefits of $50,000–$70,000 annually may need far less from their investment portfolio than they originally assumed.

A retirement income plan could look like this:

Portfolio withdrawals: $70,000

Social Security income: $55,000

Total annual spending capacity: $125,000

That is a dramatically different situation than relying entirely on investments.

This is one reason individualized retirement planning matters more than generic internet calculators.

How Do Taxes Affect Retirement With $2 Million?

Taxes can significantly impact how much retirement income you actually keep.

This is where many simplified retirement calculators fail.

Not all retirement dollars are taxed the same way.

Important questions include:

Is the money in taxable brokerage accounts?

Traditional IRA or 401(k) accounts?

Roth retirement accounts?

Real estate investments?

Business interests?

Someone with most of their wealth inside pretax retirement accounts may owe substantial taxes on withdrawals.

Meanwhile, a retiree with significant Roth savings may keep far more spendable income.

A transparent advisor will generally explain these tradeoffs clearly instead of relying on vague assumptions or overly optimistic projections.

Advice-only planners often emphasize education and implementation strategy so clients understand the financial decisions being made rather than simply delegating everything blindly. (Nowacki, 2026)

Should my retirement plan include healthcare costs?

Absolutely.

Healthcare is one of the most commonly underestimated retirement costs.

Before age 65, private health insurance can be extremely expensive.

After age 65, Medicare helps, but it does not eliminate healthcare expenses entirely.

Retirees still face:

Medicare premiums

Supplemental insurance costs

Prescription expenses

Dental and vision care

Long-term care uncertainty

A retirement plan that ignores healthcare costs often looks far better on paper than it feels in real life.

Why Does Inflation Matter So Much in Retirement?

Because retirement may last 25–35 years.

Even modest inflation compounds over time.

A lifestyle that costs $90,000 today may cost dramatically more two decades from now.

This creates an important challenge for retirees:

You need enough portfolio growth to help preserve purchasing power over time.

That is why many retirees cannot simply move entirely into cash and “play it safe.” Too little long-term growth can become a serious risk during retirement.

How Should a $2 Million Retirement Portfolio Be Invested?

The better question is not: “Can I retire on $2 million?”

It is: “How is the $2 million invested?”

Consider three simplified examples:

Scenario 1: Extremely Conservative Portfolio

If the portfolio sits mostly in low-yield cash equivalents, inflation may gradually erode purchasing power over time.

Scenario 2: Overly Aggressive Portfolio

If the portfolio experiences a severe market decline early in retirement, sustainability can become much harder.

Scenario 3: Balanced Portfolio

A diversified portfolio aligned with spending needs, taxes, time horizon, and risk tolerance may provide a stronger long-term probability of success.

A transparent financial planner should explain why recommendations exist instead of asking clients to blindly trust the process.

Transparency around assumptions, costs, and risks tends to improve client understanding and trust. (Huhulea, 2026)

What Is the Biggest Variable in Retirement Success?

Usually spending behavior.

Retirement outcomes are often more behavioral than mathematical.

Someone with $2 million who spends intentionally may retire comfortably.

Someone with $2 million experiencing continual lifestyle inflation may struggle financially despite having substantial assets.

Questions worth asking include:

How much do I spend today?

Will retirement spending increase or decrease?

Will travel costs rise?

Will I financially support adult children?

Will housing costs decrease?

What happens if markets decline?

Effective retirement planning means confronting these questions honestly rather than avoiding them.

Should You Compare Your Retirement Number to Other People?

Probably not.

There are households stressed with $5 million.

There are households thriving with $1 million.

A transparent financial advisor— especially one operating on a flat-fee, hourly, or advice-only basis — will often focus more on cash flow, taxes, tradeoffs, and planning flexibility than on portfolio vanity metrics or product sales.

These advisory models frequently emphasize fiduciary planning and transparent pricing instead of commissions or percentage-based compensation structures.

So, Can You Comfortably Retire on $2 Million?

For many Americans, yes.

But not because an online calculator says so.

Retirement may work well if:

Your spending is realistic

Taxes are planned carefully

Healthcare costs are accounted for

Investments support long-term inflation needs

Withdrawal assumptions remain flexible

Expectations align with reality

The most honest answer is this:

$2 million is enough for some people to retire comfortably and nowhere near enough for others.

Retirement planning is personal.

And if someone claims there is a universal answer without first asking about your spending, taxes, goals, family situation, and risk tolerance, they are probably oversimplifying the conversation.

If you are seeking to work with someone like me, here’s more about how I help people.

As an advice only planner, we don’t earn a fee based on the amount of assets you have with us. Instead we charge a flat fee that is based on the amount of resources and time required to serve you. This is very different from how most other advisors operate. If you’d like to discuss us helping you with your finances, let us know.

If you're searching for a:

Fee-only advisor in Princeton, New Jersey

Flat-fee planner near Princeton, NJ

Retirement planner in Princeton NJ

Fiduciary financial advisor in Mercer County

Advice-only financial planner in Princeton, NJ

…I’d be happy to help.

Thanks for reading!

— Michael

Michael Hart, CFP® is an advice-only financial planner for mid-career professionals in Princeton, New Jersey.

P.S.

We are fee-only, flat fee advisors in Princeton, NJ who help mid-career professionals build wealth. If you’d like to meet with us to discuss retiring in New Jersey, how to create a financial plan for retirement, or any other topics related to your wealth, please set up a time.

Sources

Nowacki, Lauren. (2026, May 1st). The Wall Street Journal. (n.d.). Advice-only financial advisors. WSJ Buy Side. https://www.wsj.com/buyside/personal-finance/financial-advisors/advice-only-financial-advisors

Huhulea, Irene. (2025, February 28th). Investopedia. How radical transparency can help independent advisors boost success. https://www.investopedia.com/how-radical-transparency-can-help-independent-advisors-boost-success-5196163

OpenAI. (2026). ChatGPT (GPT-5.2) [Large language model]

Disclaimer

Advice Only, Public Benefit Corporation, dba Open Book Financial Planning, is an investment adviser registered with the Securities and Exchange Commission (CRD# 334039 / SEC File No. 801-135290). Our current disclosures, including Form ADV Part 2 and Form CRS, are available on our website at www.adviceonly.com